Public Adjuster vs. Attorney: Which Do I Actually Need?

Florida public adjuster vs. attorney: the real differences, when each is the right fit, and why many Florida claims benefit from both.

Blog list

Plain-language guides from 21 years of Florida claim work: statutes explained, denial patterns, appraisal mechanics, and after-action notes from each season.

Florida public adjuster vs. attorney: the real differences, when each is the right fit, and why many Florida claims benefit from both.

Florida hurricane prep from the claims perspective: policy review, documentation, deductibles, and the pre-season checklist that saves a claim.

The first 72 hours after a Florida residential fire: safety, mitigation, documentation, and the insurance-side steps that protect the claim.

How to read a Florida homeowner insurance declarations page: coverage limits, deductibles, endorsements, and what each line actually means.

The most common Florida homeowner insurance myths that lead to underpayment or denied claims: debunked with statute and case law.

Florida roof claim denials follow predictable patterns: wear-and-tear, cosmetic exclusions, late notice. How to reverse each one.

Florida denial letters follow a template. Learn to identify the cited basis, the statutory provision, and your paths to reversal.

Florida appraisal vs. litigation: the cost, timeline, and outcome differences, and how to choose the right path for your specific dispute.

The 18-month Florida supplemental window (Fla. Stat. 627.70132) is underused. When to file, what to include, and how it preserves recovery.

SB 2A, SB 2D, HB 837: how the 2022-2023 Florida property insurance reform package reshaped the claim landscape for policyholders.

Florida bad-faith insurance explained: statutory basis (Fla. Stat. 624.155), CRN process, damages available, and how to document.

Get the most out of your free Florida public adjuster consultation: what to bring, what to ask, and what to expect.

Late notice, wrong deductible interpretation, throwing away damaged materials, accepting first offers: the claim-killing mistakes Florida homeowners make after a hurricane and how to avoid each.

Florida sinkhole claim coverage, documentation, and dispute resolution: the 2-year limitations, neutral evaluator option, and typical outcomes.

Florida insurance claim timelines explained: statutory deadlines, typical resolution windows, and what drives delays.

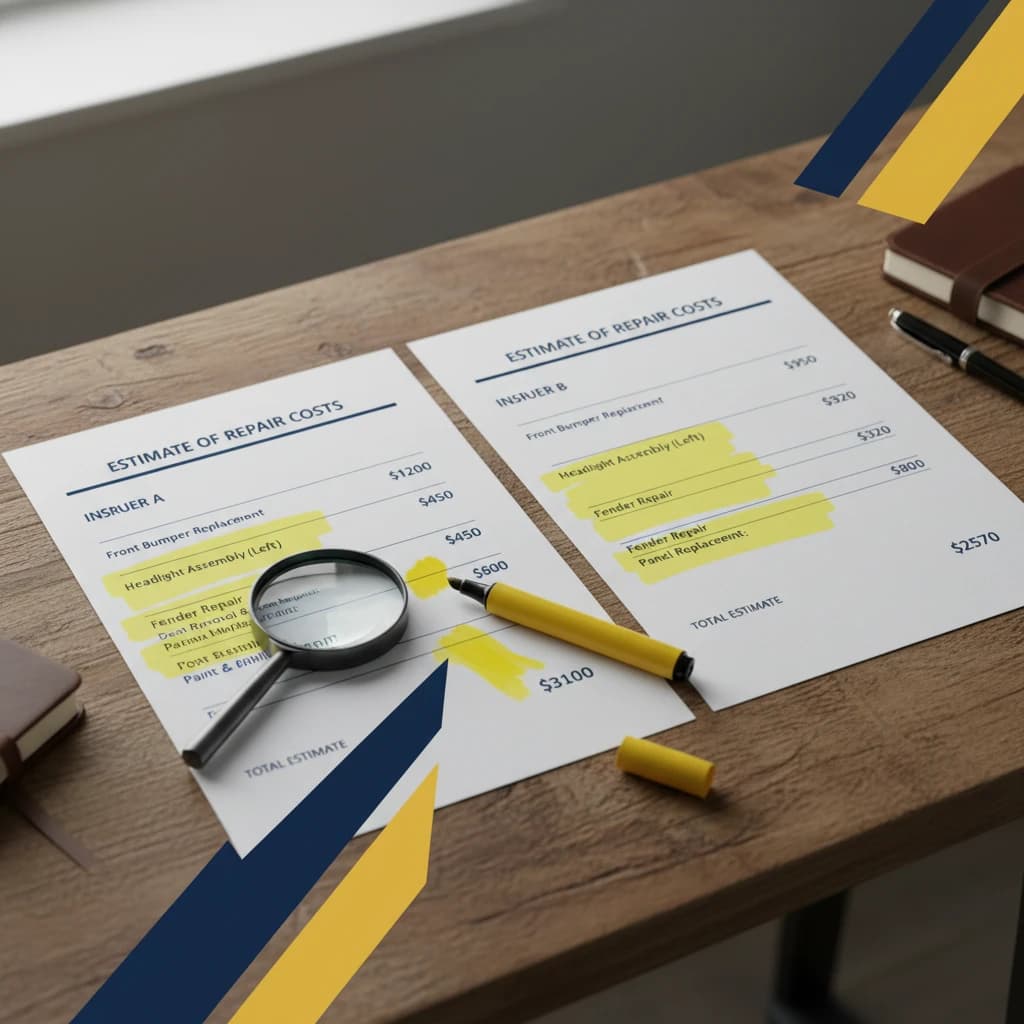

Xactimate is the estimating platform Florida carriers use. Understanding it helps you audit claim estimates and counter underpayment.

Florida carriers steer policyholders to preferred contractors. You have the right to choose your own. Here's why it matters.

Appraisal is usually a policyholder tool. But carriers invoke it too: sometimes strategically. How to respond.

Fla. Stat. 626.9744 requires continuous-area replacement when damaged materials can't be matched. One of Florida's strongest pro-policyholder statutes.

How Florida carriers inflate depreciation to reduce ACV payouts, and how to push back with documentation and statute.

Step-by-step Florida hurricane damage documentation: what to capture, when, and how to organize it for maximum claim recovery.

How Florida hurricane deductibles actually work: when they apply, how they're calculated, and what they cost you out of pocket.

How mortgage companies get named on Florida insurance claim checks, and how to navigate the endorsement process.

Fla. Stat. 627.7152 reshaped Assignment of Benefits after 2022 reform. What's permissible, what isn't, and what policyholders should do.

Florida first-party (your own claim) vs. third-party (liability) insurance claims: the critical differences and how each is handled.

Florida DFS-sponsored mediation walkthrough: what happens on the day, how to prepare, and typical outcomes.

Hidden moisture in Florida walls is the most commonly underpaid water-damage scope. How to detect and document.

Inside carrier SIU (Special Investigations Unit) fraud-handling: triggers, process, and how legitimate claims get caught up.

Florida condominium insurance disputes between unit owners and associations: coverage boundaries, documentation, and resolution paths.

When a Florida insurance carrier becomes insolvent, policyholders face specific risks and protections. What happens and how FIGA handles claims.

Hurricane Ian hit in September 2022. Three years on, what claim options remain for Florida policyholders still dealing with post-Ian issues.

How to pick a Florida contractor for insurance-claim repair work: licensing, experience, AOB avoidance, and red flags to watch.

Company adjusters, independent adjusters, public adjusters, and catastrophe adjusters: the legal and practical differences in Florida.

Every stage of a Florida property insurance claim with expected timing, statutory deadlines, and what can slow things down.

Florida commercial business interruption coverage: what's covered, how lost income is calculated, and the claim process.

Every aspect of a Florida residential fire insurance claim: from first call to final settlement, with the statutes and tactics that matter.

HVAC damage from storms, water, lightning, and smoke: the claim issues, coverage basis, and replacement-vs-repair dispute.

How Florida hurricane claims work in 2026: the hurricane deductible, the 60-day pay-or-deny rule (Fla. Stat. 627.70131), and the 1-year notice deadline.

The costly property insurance claim mistakes Florida homeowners make, from missing the 1-year notice deadline (Fla. Stat. 627.70132) to accepting the first offer.

Maximize a Florida property insurance claim: document fully, read your policy, claim matching (Fla. Stat. 626.9744) and code upgrades, and enforce carrier deadlines.

A Florida public adjuster represents the policyholder, not the insurer, licensed under Fla. Stat. 626.854 to document, estimate, and negotiate your claim.

Vero Beach water intrusion claims hinge on proving a wind-created opening. How Indian River County coastal claims get disputed, and how to protect your settlement.

Why West Palm Beach storm claims come in low: underscoped roofs, omitted matching (Fla. Stat. 626.9744), and missed code upgrades. How to recover the difference.

Inland Sebring roof damage is often underscoped after storms. What Highlands County homeowners should document to protect a roof insurance claim.

The hurricane claim mistakes that cost Fort Myers homeowners: trusting the first inspection, overlooking roof damage, and missing the 1-year notice deadline.

A step-by-step guide for Orlando homeowners after hurricane or storm damage: document, mitigate, understand your hurricane deductible, and meet the filing deadline.

Condo or HOA on the Treasure Coast? Florida Statute 718.111(11) splits the master policy from your HO-6. Who pays for roof, water, and interior damage explained.

Dispute an underpaid Florida claim: review the policy, build an independent estimate, then use appraisal, DFS mediation, or a Civil Remedy Notice (Fla. Stat. 624.155).

What is a CAT adjuster? A catastrophe adjuster is hired by your insurer after a hurricane to process claims fast. Learn how they differ from a public adjuster.

Should you hire a public adjuster in Florida? When representation pays off on a denied, underpaid, or delayed claim, what it costs, and when you may not.

How COVID-era business interruption claims were evaluated in Florida, why viral-loss exclusions applied, and what to check in your BI policy language.

Denied or underpaid Florida claim? A licensed public adjuster re-estimates the loss and negotiates, on a fee capped by Fla. Stat. 626.854. How it works.

Eli Goins, an expert at Ocean Point Claims, brings his expertise to fire insurance claims. Pursue the full value your policy supports with Eli Goins by your side.

Ocean Point's Eli Goins was featured by CBS News on Florida's property insurance reform. What the bill changed for policyholders and claim deadlines.

The most common Florida property damage claims, water, wind, roof, and fire, and why each is frequently underpaid. What policyholders should document.

Discover why Florida homeowners should hire experienced public adjusters to navigate denied and underpaid insurance claims effectively. Learn how Florida public adjusters advocate, negotiate, and pursue the full value the policy supports, ensuring fair treatment and peace of mind.

If your home or business was damaged by Hurricane Idalia, call Ocean Point Claims to get help with the insurance claims process.

Navigate the time-sensitive challenge of filing Hurricane Ian insurance claims, where homeowners have less than a year left out of the two-year timeframe. Trust our experts to address underpaid or denied claims and pursue the full value your policy supports.

Documentation, mitigation, and policy review steps every Florida homeowner and business owner should complete before filing a water damage insurance claim, with carrier-side pitfalls to avoid.

The types of insurance adjusters explained, company, independent, and public, and whose interests each represents in a Florida property claim.

Receiving an undisputed payment, even if it’s not enough to cover the full cost of repair, does not mean this is the end of your insurance claim.

Florida property claims must be reported within 1 year of loss and supplemented within 18 months under Fla. Stat. 627.70132. The deadlines explained.

If your home or business was damaged by a hurricane, call Ocean Point Claims to get help with the insurance claims process.

Your mortgage company is named on your Florida insurance claim check as lienholder. How to get it endorsed: the loss draft department, escrow over $40,000, and lost or incorrect checks.

Steps you should take after a fire. Fire damage to your property is stressful. The task of taking on the insurance company alone is daunting!

Hurricane Milton's October 2024 path across Florida and the claim-handling dynamics that followed. What affected homeowners should know about recovery.

Hurricane Milton spawned tornadoes that compounded Florida storm damage in October 2024. How multi-peril claims are documented and why they get disputed.

Article indexes for our most-published claim categories.

Pipe burst, slab leak, supply-line failure, and storm-driven water intrusion claims.

Hurricane, wind, hail, and named-storm property claim coverage.

How public adjusting works, fees, when to hire, what to expect.

Free claim review. No recovery, no fee. Answered 24/7.

Get a free claim review