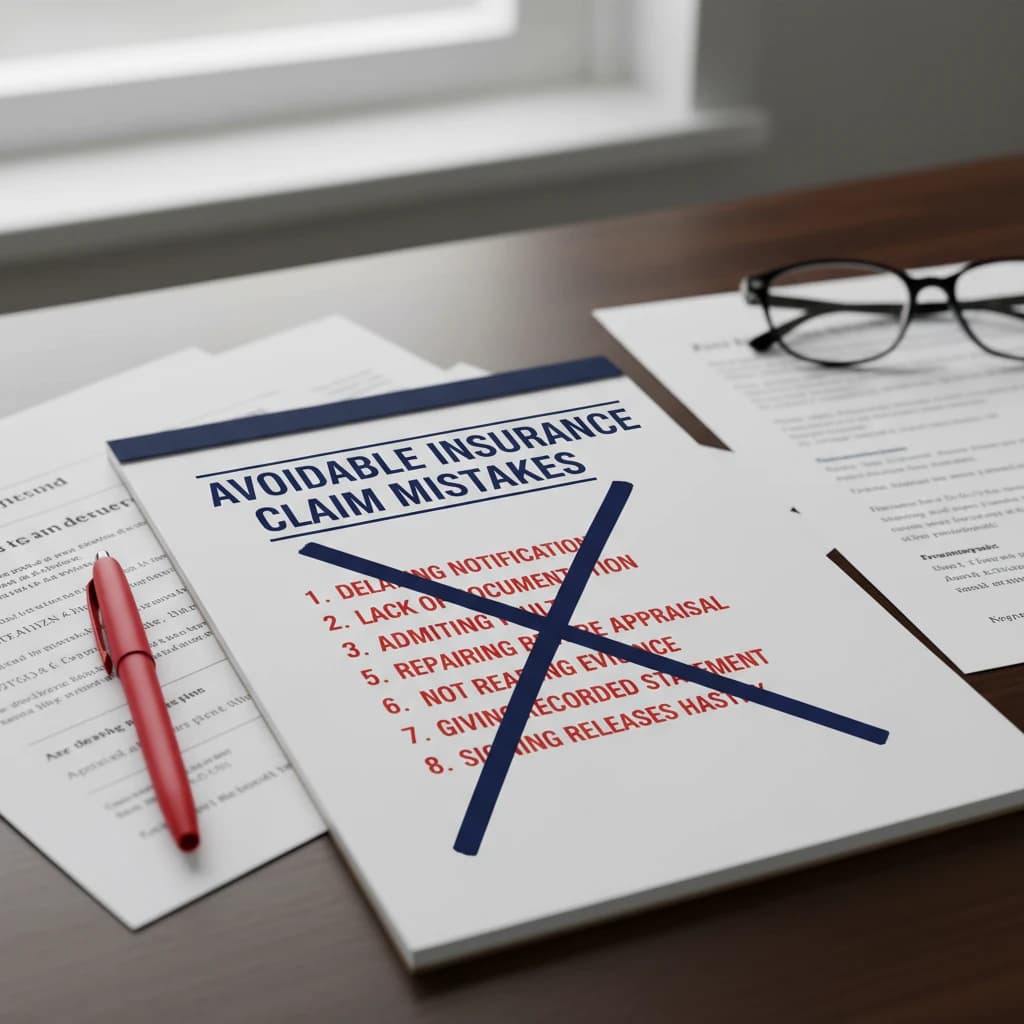

Short answer: The most common Florida claim mistakes are documenting damage too late, missing hidden damage, blowing the 1-year notice deadline under Fla. Stat. 627.70132, accepting the carrier's first estimate, and giving a recorded statement without preparation. Each one quietly lowers the settlement, and each one is avoidable.

Mistake 1: Waiting too long to document

After a loss, the condition of your property is evidence. Photograph and video everything before any cleanup or repair. Delay lets the carrier argue the damage predated the event or worsened from neglect. A timestamped photo set taken within 24 to 72 hours is the single strongest record you can build.

Mistake 2: Missing hidden damage

The damage that lowers settlements most is the damage you cannot see from the floor:

- Roof decking and underlayment moisture

- Wind-driven rain inside wall cavities

- Structural shifting after wind load

- Mold developing behind baseboards

A quick adjuster walkthrough rarely captures these. Attic inspection, moisture meters, and sometimes an infrared scan are what move them onto the estimate.

Mistake 3: Missing the statutory deadline

Many homeowners still believe they have years to file. Under Fla. Stat. 627.70132, a new or reopened claim must be reported within 1 year of the date of loss, and a supplemental within 18 months. Wait past those windows and most claims are time-barred, no matter how valid.

Mistake 4: Accepting the first offer

The carrier's first estimate is an opening position, not a final number. It frequently omits matching (Fla. Stat. 626.9744), code-upgrade costs, and overhead and profit. Compare it line by line against an independent Xactimate estimate before you cash anything. Endorsing a check can be treated as accepting the settlement.

Mistake 5: Giving an unprepared recorded statement

Carriers may request a recorded statement early. Casual, speculative answers about when damage "probably" started can be used to recharacterize a covered loss as wear and tear. Stick to facts you know.

Mistake 6: Throwing away damaged property too soon

Homeowners often haul damaged materials to the curb before the carrier inspects. Once the evidence is gone, the carrier can dispute that the damage existed or its extent. Keep damaged items, or at minimum a thorough photo and video record with model numbers, until the claim is resolved. Florida policies require you to protect the property from further damage, not to discard the proof.

Mistake 7: Ignoring the duties-after-loss clause

Every Florida policy has a duties-after-loss section: prompt notice, mitigation, a sworn proof of loss if requested, and cooperation with the carrier's investigation. Missing one of these gives the carrier a procedural reason to delay or deny, separate from the merits of the damage. Read that clause early and calendar every request.

Mistake 8: Going it alone on a disputed claim

You can negotiate yourself, but on a contested claim the carrier has staff adjusters and engineers on its side. A licensed public adjuster represents only you, builds the independent estimate, and runs appraisal or mediation if needed. Fees are capped by Fla. Stat. 626.854, generally up to 20% of the claim payment and 10% for declared-emergency claims in the first year.

How these mistakes compound

No single mistake usually sinks a claim; it is the stack. A late, thin photo set makes hidden damage easy to dispute, which makes the first offer low, which a homeowner then accepts because the supplemental deadline feels far off, until it isn't. Breaking the chain anywhere, documenting early, reading the policy, refusing the first number, protects the rest. The homeowners who recover the most treat the claim as a project with a paper trail, not a single phone call.

What to do next

If you suspect your claim was underscoped or you are approaching a deadline, get a second set of eyes before you sign. Call (888) 824-1306 or request a free claim review.